The Australian Energy Regulator (AER)'s draft decision on the 2026 Rate of Return Instrument will be one of the highest-impact decisions for household energy bills in the coming years. If these changes are implemented in the Final Decision, the AER estimates this will save consumers around $1.1 billion over the coming years.

The draft is a positive step and reflects long-standing advocacy from Energy Consumers Australia. However, there remains scope to reduce the rate of return further while still supporting efficient investment.

With energy bills remaining a key concern for consumers and governments, it is critical that the rate of return is set no higher than necessary. Getting this right is essential to ensuring the energy transition delivers not just cleaner energy, but more affordable power for Australian households.

Have your say

Are you an advocate who wants to see fairer energy prices for consumers? Make sure to have your say on the AER's 2026 RORI draft decision before the submission deadline, 31 July 2026.

If you have any questions about the process or what to include in your submission, get in touch.

What is the rate of return and why is it important?

Network costs account for around 39 to 45 per cent of electricity costs for households in the National Electricity Market (NEM). Network costs are generally the largest component of consumer electricity bills and have grown materially in some jurisdictions in recent years.

The rate of return, set by the AER, determines how much network businesses can earn on their capital investments. It is essentially the “interest rate” consumers pay networks for their investment in infrastructure such as poles, wires and substations.

The rate of return sets around 40 to 60% of network costs and is likely the single largest driver of household energy bills. The AER has acknowledged that increased rates of return have been a primary driver of rising revenue forecasts for multiple networks, including Ausgrid, Endeavour Energy, Essential Energy and TasNetworks.

If set too low, networks may not invest in their infrastructure, causing risks to the safety and reliability of supply. If set too high, consumers pay more than necessary for network services. Further, if the regulated rate of return is higher than a business’s underlying cost of capital, this can encourage over-investment. This is because network businesses have an incentive to invest more than necessary to earn higher returns.

Looking ahead, network capital expenditures are forecast to rise materially. For example, AusNet Services forecasts total Victorian transmission revenues will nearly triple over the next decade. The AER’s final determination for Energex and Ergon Energy included capex allowances that were 30 and 62 per cent higher than the previous period. It is vital for network returns not to create incentives for networks to spend more than necessary to chase higher earnings.

Has the AER set the rate of return at the right level?

In essence, the AER must determine the level that ensures networks can invest in their infrastructure, while not setting it so high that consumers pay more than necessary. Below, we investigate whether the AER’s rate of return has been appropriately set.

The current rate of return is not constraining network investment

In the AER’s own assessment there is "no evidence that [the rate of return instrument] has deterred investment... with network businesses continuing to propose capital expenditure and innovation allowance projects."

One way to assess whether investment is deterred is to compare forecast capital expenditure with actual expenditure. If the rate of return were too low, networks would face constraints in financing their capital programs, leading to underspending relative to forecasts.

The AER also operates the Capital Expenditure Sharing Scheme (CESS) which provides financial incentives for networks to underspend relative to their approved allowances. Further, the CESS may also encourage networks to over-forecast capital expenditure, as it makes underspending easier.

Therefore, if networks are still spending close to forecast capital expenditure even with these incentives, it is difficult to argue that the rate of return is constraining investment.

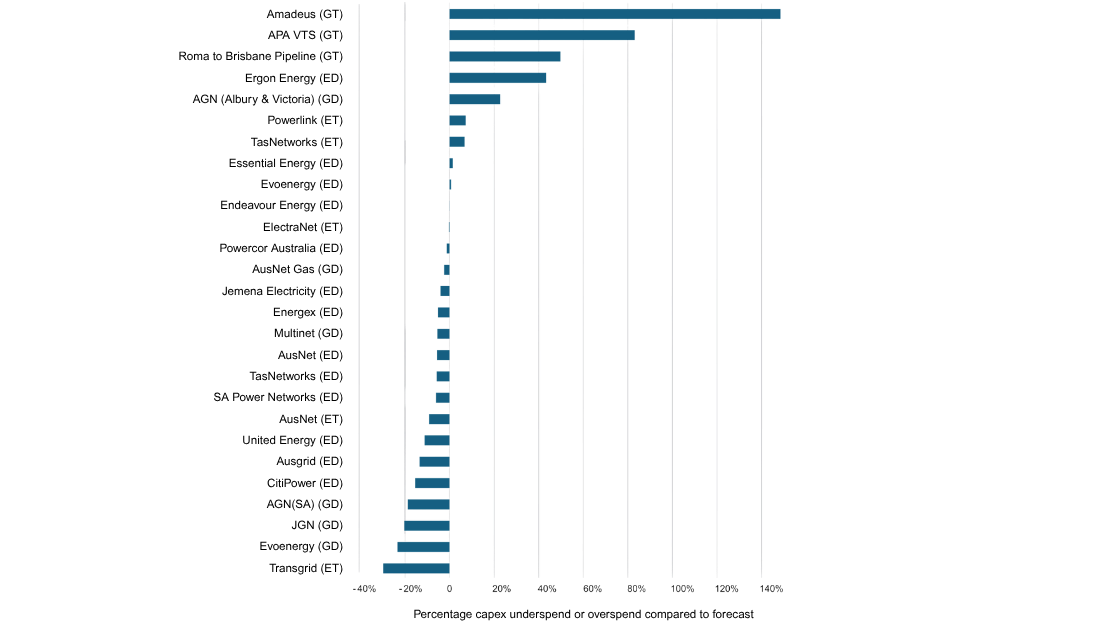

Figure 3 shows the extent to which networks have under- or overspent on their capital expenditure forecasts over the last five years. Of the 27 networks regulated by the AER:

- 9 networks overspent on forecast capital

- 11 networks underspent by less than 10%

- 7 networks underspent by more than 10%

These outcomes show a wide dispersion rather than a consistent pattern of underspending, which would be expected if the rate of return was preventing investment.

Figure 3: Percentage difference between actual capital expenditure from forecast for regulated energy networks over the last five years

Source: ECA analysis of AER Network operational performance data. Accessed here. Note: G means gas network and E is electricity network. T means transmission and D is distribution.

The current rate of return is higher than necessary to support investment

Currently, the AER determines the rate of return using a bottom-up methodology. The AER’s 2022 Consumer Reference Group argued that several parameter settings were upwardly biased.

One key input is the equity beta, which measures how much a company’s returns move with the overall market. The higher the beta, the higher the perceived investment risk, and therefore the higher the rate of return and earnings for the network.

For example, a low beta (around 0.3) means returns are very stable, while a beta of 1 means returns move in line with the market. Regulated energy networks are monopoly service providers operating under stable regulatory frameworks. This generally results in lower exposure to market risk than firms operating in competitive markets, which should be reflected in a lower equity beta.

The AER currently adopts an equity beta of 0.6, based on analysis of publicly available equity beta estimates from comparative businesses. However, analysis for Energy Consumers Australia by Electricity Market Advisory Services (EMAS) indicates that this sample includes firms that are not predominantly regulated monopolies. If the AER were to exclude these non-representative businesses from the benchmarking analysis, the estimated equity beta would be closer to 0.4.

The AER’s draft decision

The AER’s draft decision has updated several parameters, including equity beta and the market risk premium. Notably, the AER has set equity beta at 0.55, reflecting an updated benchmarking analysis.

The AER estimates that changes to equity beta and the market risk premium will deliver an aggregate reduction in regulated revenues of around $1.1 billion to consumers via upcoming regulatory revenue determinations.

While the AER should be commended for making these changes, they represent an incremental evolution of the existing framework, rather than a material shift in how the rate of return is determined.

We believe that an equity beta of 0.55 is still above what the evidence supports. This means there are further opportunities to reduce the rate of return and deliver millions of dollars in savings for consumers.

Equity beta is just one key issue we have raised for the AER to consider. Readers can see the EMAS report for an analysis of these issues here.

As a result, key questions—particularly around the risks faced by regulated networks and whether current settings appropriately compensate those risks—are likely to remain central issues ahead of the final decision.

Make a submission

For further information, see the AER’s Draft Rate of Return Instrument Decision here. Submissions to are due to the AER on 31 July 2026.

This article originally appeared in Renew Economy.

FAQs

The rate of return, set by the AER, determines how much network businesses can earn on their capital investments. Given that network costs can account for as much as 45% (and growing) of electricity bills for households in the National Electricity Market (NEM), the impact of changes to network earnings has the potential to be very significant. The Australian Energy Regulator estimates changes proposed in its draft decision on the 2026 Rate of Return Instrument will save consumers around $1.1 billion over the coming years.

We think these proposed changes can be further strengthened. That's why we're calling on consumer advocates to join us by making a submission to the draft decision before the submission deadline on 31 July 2026. If you're an advocate with questions about this process, contact us.

Consumer advocates can influence this process in a number of key ways, namely:

- Making a submission to the draft 2026 Rate of Return Instrument (RORI) by no later than 31 July 2026 via the AER's website.

- Talking about RORI within your organisation, and why it matters for consumers.

- Contacting us to find out more about RORI and what you can do.

For any questions about the process and what to include in your submission, get in touch.